To get more information on Pressure Ulcer Treatment Market - Request Sample Report

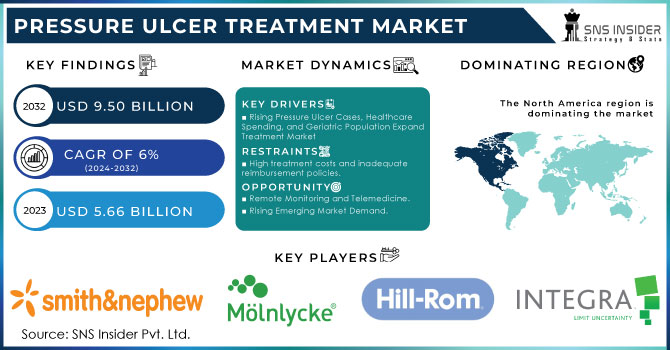

The Pressure Ulcer Treatment Market size was valued at USD 5.66 billion in 2023 and is expected to reach USD 9.50 billion by 2032 at a CAGR of 6% during the forecast period of 2024-2032.

The increase in the older population with chronic sickness and physical disabilities caused by pressure ulcers has created a need in the medical business for relevant therapies. Managing and treating pressure ulcers is one of the key elements driving the pressure ulcer treatment landscape. Furthermore, despite the fact that various healthcare providers in the business offer many breakthrough wound care equipment, dressings, and therapies, it is becoming a Gordian knot for healthcare institutions, including hospitals and community health centers.

Because treating pressure ulcers is significantly more expensive than preventing them, the field of pressure ulcer treatment is shifting toward preventative care approaches. Hospitals and healthcare facilities are employing cutting-edge movement tracking systems to improve patient care by reducing pressure ulcers. Furthermore, as new technologies develop to support the healthcare sector's digital transformation, digital parts of pressure ulcer avoidance systems are becoming more prevalent. With increasing awareness of the negative effects pressure ulcers have on patients' health and quality of life, demand for pressure ulcer remedies is predicted to rise by double digits.

DRIVERS

An increase in the number of patients with pressure ulcers, rising healthcare expenditure, an increase in the geriatric population, an increase in the adoption of artificial skin substitutes, rising government funding, and rising initiatives by government and private organizations to raise awareness about the negative impact of pressure ulcers on patient health and quality of life are all factors that will expand the pressure ulcer treatment market.

Increased R&D activities, significant unmet demands, and the development of therapeutic and diagnostic technologies will present favorable possibilities for the pressure ulcer treatment market between 2024 and 2031.

RESTRAIN

High treatment costs and inadequate reimbursement policies.

During the projection period, the high cost of treatment and unfavorable reimbursement policies in low-income countries would hamper market expansion and represent further difficulties for the pressure ulcer treatment market. Pressure ulcer treatment reimbursement is relatively limited, especially for novel and innovative treatments. Furthermore, such therapies are not covered by insurance, making it difficult for healthcare professionals to grant payment in such cases.

OPPORTUNITY

Remote Monitoring and Telemedicine.

Rising Emerging Market Demand.

Regenerative and personalized therapies.

CHALLENGES

Patient Compliance, Infection Control, and Limited Reimbursement Policies.

Infection is a major concern in the management of pressure ulcers. Infection prevention and management in these wounds can be difficult and may necessitate specialist techniques. Inadequate remuneration for pressure ulcer treatment and prevention initiatives can have an impact on healthcare providers' desire to invest in high-quality care. Effective pressure ulcer therapy frequently necessitates persistent patient compliance with wound care techniques, which can be difficult, especially in home settings.

Disruption in Healthcare Infrastructure Geopolitical wars, such as the one raging between Russia and Ukraine, can impair healthcare infrastructure, including hospitals, clinics, and medical supply networks. This disruption may have an impact on the availability and distribution of pressure ulcer therapy and wound care products. Conflict can interrupt the supply chain for medical products and equipment, potentially resulting in shortages of wound care supplies, specialty mattresses, and other devices used in pressure ulcer therapy.

IMPACT OF ONGOING RECESSION

Purchases that have been postponed or reduced Hospitals and healthcare facilities may postpone or restrict the procurement of medical equipment and supplies, particularly those used to treat pressure ulcers. Capital-intensive investments may be postponed, reducing demand for specialized pressure ulcer treatment devices and goods. Priorities in Healthcare Have shifted. Recessions can cause healthcare providers to prioritize cost-effective and important treatments. Pressure ulcer prevention and treatment may be prioritized over more urgent or life-threatening illnesses, affecting wound care resources. Disruptions in the Supply Chain Economic downturns can disrupt global supply chains, reducing the availability of pressure ulcer treatment supplies and wound care treatments. Shortages or delays in getting these goods may have an effect on patient care.

By Product Type

Wound Care Dressing

Other

By Type

Stage 1

Stage 2

Stage 3

Stage 4

By End-User

Clinics

Hospital

Homecare Settings

REGIONAL ANALYSES

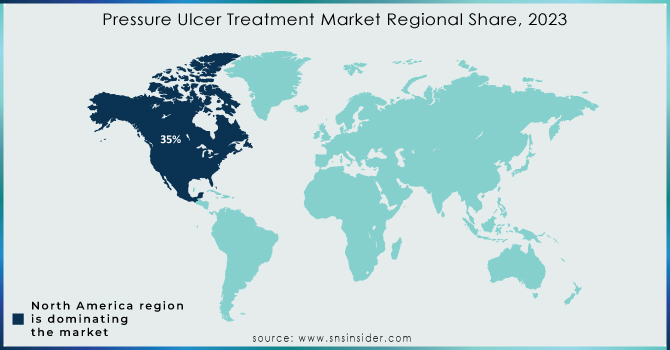

North America will account for approximately 35% of the worldwide pressure ulcer therapy market. From 2024 to 2031, the region's market is expected to increase at a CAGR of 5.4%. Factors propelling the market in North America and Europe include an increase in the elderly population, an increase in the frequency of chronic diseases, and technological improvements.

During the projected period, Asia-Pacific is expected to be the fastest-growing region of the global market. The region's pressure ulcer treatment market is benefiting from increased awareness. During the forecast period, the Asia-Pacific market is expected to increase at a CAGR of 6.1%. The market in the Middle East and Africa, as well as Latin America, is expected to rise moderately in the near future. This is due to an increase in demand for wound dressings and artificial skin products in these areas.

Get Customized Report as per your Business Requirement - Request For Customized Report

REGIONAL COVERAGE

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

The major players are Smith & Nephew plc, Integra LifeSciences, Hill-Rom Holdings, Inc, Mélnlycke Health Care AB, Essity Aktiebolag, Cardinal Health, 3M, B. Braun Melsungen AG, Acelity LP., Inc., Coloplast Group, ConvaTec Group ple and others.

Michelin debuted MICHELIN: In 2022, Michelin debuted MICHELIN AirProne at the Intensive Care Show 2022 in June 2022. Cushion set designed for people suffering from acute respiratory distress syndrome (ARDS).

| Report Attributes | Details |

| Market Size in 2023 | US$ 5.66 Bn |

| Market Size by 2032 | US$ 9.50 Bn |

| CAGR | CAGR of 6% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Wound Care Devices, Wound Care Dressing, Other) • By Type (Stage 1, Stage 2, Stage 3, Stage 4) • By End-User (Clinics, Hospital, Homecare Settings, Ambulatory Surgical Centers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]). Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Smith & Nephew plc, Integra LifeSciences, Hill-Rom Holdings, Inc, Mélnlycke Health Care AB, Essity Aktiebolag, Cardinal Health, 3M, B. Braun Melsungen AG, Acelity LP., Inc., Coloplast Group, ConvaTec Group ple |

| Key Drivers | • An increase in the number of patients with pressure ulcers, rising healthcare expenditure, an increase in the geriatric population, an increase in the adoption of artificial skin substitutes, rising government funding, and rising initiatives by government and private organizations to raise awareness about the negative impact of pressure ulcers on patient health and quality of life are all factors that will expand the pressure ulcer treatment market. |

| Market Restraints | • High treatment costs and inadequate reimbursement policies. |

Ans: The Pressure ulcer treatment market is expected to grow at 6% CAGR from 2024 to 2031.

Ans: According to our analysis, the Pressure ulcer treatment market is anticipated to reach USD 9.50 billion By 2032.

Ans: The leading participants in the, Smith & Nephew plc, Integra LifeSciences, Hill-Rom Holdings, Inc, Mélnlycke Health Care AB, Essity Aktiebolag, Cardinal Health, 3M.

Ans: The global pressure ulcers treatment market is being driven by an increase in the number of patients suffering from pressure ulcers as well as increased knowledge regarding pressure ulcers and their treatment.

Ans: Yes, you may request customization based on your company's needs.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 Impact of the Ukraine- Russia War

4.2 Impact of Ongoing Recession

4.2.1 Introduction

4.2.2 Impact on major economies

4.2.2.1 US

4.2.2.2 Canada

4.2.2.3 Germany

4.2.2.4 France

4.2.2.5 United Kingdom

4.2.2.6 China

4.2.2.7 Japan

4.2.2.8 South Korea

4.2.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Pressure ulcer treatment market, By Product Type

8.1 Wound Care Devices

8.2 Wound Care Dressing

8.3 Other

9. Pressure ulcer treatment market, By Type

9.1 Stage 1

9.2 Stage 2

9.3 Stage 3

9.4 Stage 4

10. Pressure ulcer treatment market, By End-User

10.1 Clinics

10.2 Hospital

10.3 Homecare Settings

10.4 Ambulatory Surgical Centers

11. Regional Analysis

11.1 Introduction

11.2 North America

11.2.1 North America Pressure ulcer treatment market by country

11.2.2North America Pressure ulcer treatment market by Product

11.2.3 North America Pressure ulcer treatment market by Type

11.2.4 North America Pressure ulcer treatment market by End-user

11.2.5 USA

11.2.5.1 USA Pressure ulcer treatment market by Product

11.2.5.2 USA Pressure ulcer treatment market by Type

11.2.5.3 USA Pressure ulcer treatment market by End-user

11.2.6 Canada

11.2.6.1 Canada Pressure ulcer treatment market by Product

11.2.6.2 Canada Pressure ulcer treatment market by Type

11.2.6.3 Canada Pressure ulcer treatment market by End-user

11.2.7 Mexico

11.2.7.1 Mexico Pressure ulcer treatment market by Product

11.2.7.2 Mexico Pressure ulcer treatment market by Type

11.2.7.3 Mexico Pressure ulcer treatment market by End-user

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Eastern Europe Pressure ulcer treatment market by country

11.3.1.2 Eastern Europe Pressure ulcer treatment market by Product

11.3.1.3 Eastern Europe Pressure ulcer treatment market by Type

11.3.1.4 Eastern Europe Pressure ulcer treatment market by End-user

11.3.1.5 Poland

11.3.1.5.1 Poland Pressure ulcer treatment market by Product

11.3.1.5.2 Poland Pressure ulcer treatment market by Type

11.3.1.5.3 Poland Pressure ulcer treatment market by End-user

11.3.1.6 Romania

11.3.1.6.1 Romania Pressure ulcer treatment market by Product

11.3.1.6.2 Romania Pressure ulcer treatment market by Type

11.3.1.6.4 Romania Pressure ulcer treatment market by End-user

11.3.1.7 Turkey

11.3.1.7.1 Turkey Pressure ulcer treatment market by Product

11.3.1.7.2 Turkey Pressure ulcer treatment market by Type

11.3.1.7.3 Turkey Pressure ulcer treatment market by End-user

11.3.1.8 Rest of Eastern Europe

11.3.1.8.1 Rest of Eastern Europe Pressure ulcer treatment market by Product

11.3.1.8.2 Rest of Eastern Europe Pressure ulcer treatment market by Type

11.3.1.8.3 Rest of Eastern Europe Pressure ulcer treatment market by End-user

11.3.2 Western Europe

11.3.2.1 Western Europe Pressure ulcer treatment market by Product

11.3.2.2 Western Europe Pressure ulcer treatment market by Type

11.3.2.3 Western Europe Pressure ulcer treatment market by End-user

11.3.2.4 Germany

11.3.2.4.1 Germany Pressure ulcer treatment market by Product

11.3.2.4.2 Germany Pressure ulcer treatment market by Type

11.3.2.4.3 Germany Pressure ulcer treatment market by End-user

11.3.2.5 France

11.3.2.5.1 France Pressure ulcer treatment market by Product

11.3.2.5.2 France Pressure ulcer treatment market by Type

11.3.2.5.3 France Pressure ulcer treatment market by End-user

11.3.2.6 UK

11.3.2.6.1 UK Pressure ulcer treatment market by Product

11.3.2.6.2 UK Pressure ulcer treatment market by Type

11.3.2.6.3 UK Pressure ulcer treatment market by End-user

11.3.2.7 Italy

11.3.2.7.1 Italy Pressure ulcer treatment market by Product

11.3.2.7.2 Italy Pressure ulcer treatment market by Type

11.3.2.7.3 Italy Pressure ulcer treatment market by End-user

11.3.2.8 Spain

11.3.2.8.1 Spain Pressure ulcer treatment market by Product

11.3.2.8.2 Spain Pressure ulcer treatment market by Type

11.3.2.8.3 Spain Pressure ulcer treatment market by End-user

11.3.2.9 Netherlands

11.3.2.9.1 Netherlands Pressure ulcer treatment market by Product

11.3.2.9.2 Netherlands Pressure ulcer treatment market by Type

11.3.2.9.3 Netherlands Pressure ulcer treatment market by End-user

11.3.2.10 Switzerland

11.3.2.10.1 Switzerland Pressure ulcer treatment market by Product

11.3.2.10.2 Switzerland Pressure ulcer treatment market by Type

11.3.2.10.3 Switzerland Pressure ulcer treatment market by End-user

11.3.2.11.1 Austria

11.3.2.11.2 Austria Pressure ulcer treatment market by Product

11.3.2.11.3 Austria Pressure ulcer treatment market by Type

11.3.2.11.4 Austria Pressure ulcer treatment market by End-user

11.3.2.12 Rest of Western Europe

11.3.2.12.1 Rest of Western Europe Pressure ulcer treatment market by Product

11.3.2.12.2 Rest of Western Europe Pressure ulcer treatment market by Type

11.3.2.12.3 Rest of Western Europe Pressure ulcer treatment market by End-user

11.4 Asia-Pacific

11.4.1 Asia-Pacific Pressure ulcer treatment market by country

11.4.2 Asia-Pacific Pressure ulcer treatment market by Product

11.4.3 Asia-Pacific Pressure ulcer treatment market by Type

11.4.4 Asia-Pacific Pressure ulcer treatment market by End-user

11.4.5 China

11.4.5.1 China Pressure ulcer treatment market by Product

11.4.5.2 China Pressure ulcer treatment market by Type

11.4.5.3 China Pressure ulcer treatment market End-user

11.4.6 India

11.4.6.1 India Pressure ulcer treatment market by Product

11.4.6.2 India Pressure ulcer treatment market by Type

11.4.6.3 India Pressure ulcer treatment market by End-user

11.4.7 Japan

11.4.7.1 Japan Pressure ulcer treatment market by Product

11.4.7.2 Japan Pressure ulcer treatment market by Type

11.4.7.3 Japan Pressure ulcer treatment market by End-user

11.4.8 South Korea

11.4.8.1 South Korea Pressure ulcer treatment market by Product

11.4.8.2 South Korea Pressure ulcer treatment market by Type

11.4.8.3 South Korea Pressure ulcer treatment market by End-user

11.4.9 Vietnam

11.4.9.1 Vietnam Pressure ulcer treatment market by Product

11.4.9.2 Vietnam Pressure ulcer treatment market by Type

11.4.9.3 Vietnam Pressure ulcer treatment market by End-user

11.4.10 Singapore

11.4.10.1 Singapore Pressure ulcer treatment market by Product

11.4.10.2 Singapore Pressure ulcer treatment market by Type

11.4.10.3 Singapore Pressure ulcer treatment market by End-user

11.4.11 Australia

11.4.11.1 Australia Pressure ulcer treatment market by Product

11.4.11.2 Australia Pressure ulcer treatment market by Type

11.4.11.3 Australia Pressure ulcer treatment market by End-user

11.4.12 Rest of Asia-Pacific

11.4.12.1 Rest of Asia-Pacific Pressure ulcer treatment market by Product

11.4.12.2 Rest of Asia-Pacific Pressure ulcer treatment market by Type

11.4.12.3 Rest of Asia-Pacific Pressure ulcer treatment market by End-user

11.5 Middle East & Africa

11.5.1 Middle East

11.5.1.1 Middle East Pressure ulcer treatment market by country

11.5.1.2 Middle East Pressure ulcer treatment market by Product

11.5.1.3 Middle East Pressure ulcer treatment market by Type

11.5.1.4 Middle East Pressure ulcer treatment market by End-user

11.5.1.5 UAE

11.5.1.5.1 UAE Pressure ulcer treatment market by Product

11.5.1.5.2 UAE Pressure ulcer treatment market by Type

11.5.1.5.3 UAE Pressure ulcer treatment market by End-user

11.5.1.6 Egypt

11.5.1.6.1 Egypt Pressure ulcer treatment market by Product

11.5.1.6.2 Egypt Pressure ulcer treatment market by Type

11.5.1.6.3 Egypt Pressure ulcer treatment market by End-user

11.5.1.7 Saudi Arabia

11.5.1.7.1 Saudi Arabia Pressure ulcer treatment market by Product

11.5.1.7.2 Saudi Arabia Pressure ulcer treatment market by Type

11.5.1.7.3 Saudi Arabia Pressure ulcer treatment market by End-user

11.5.1.8 Qatar

11.5.1.8.1 Qatar Pressure ulcer treatment market by Product

11.5.1.8.2 Qatar Pressure ulcer treatment market by Type

11.5.1.8.3 Qatar Pressure ulcer treatment market by End-user

11.5.1.9 Rest of Middle East

11.5.1.9.1 Rest of Middle East Pressure ulcer treatment market by Product

11.5.1.9.2 Rest of Middle East Pressure ulcer treatment market by Type

11.5.1.9.3 Rest of Middle East Pressure ulcer treatment market by End-user

11.5.2 Africa

11.5.2.1 Africa Pressure ulcer treatment market by country

11.5.2.2 Africa Pressure ulcer treatment market by Product

11.5.2.3 Africa Pressure ulcer treatment market by Type

11.5.2.4 Africa Pressure ulcer treatment market by End-user

11.5.2.5 Nigeria

11.5.2.5.1 Nigeria Pressure ulcer treatment market by Product

11.5.2.5.2 Nigeria Pressure ulcer treatment market by Type

11.5.2.5.3 Nigeria Pressure ulcer treatment market by End-user

11.5.2.6 South Africa

11.5.2.6.1 South Africa Pressure ulcer treatment market by Product

11.5.2.6.2 South Africa Pressure ulcer treatment market by Type

11.5.2.6.3 South Africa Pressure ulcer treatment market by End-user

11.5.2.7 Rest of Africa

11.5.2.7.1 Rest of Africa Pressure ulcer treatment market by Product

11.5.2.7.2 Rest of Africa Pressure ulcer treatment market by Type

11.5.2.7.3 Rest of Africa Pressure ulcer treatment market by End-user

11.6 Latin America

11.6.1 Latin America Pressure ulcer treatment market by country

11.6.2 Latin America Pressure ulcer treatment market by Product

11.6.3 Latin America Pressure ulcer treatment market by Type

11.6.4 Latin America Pressure ulcer treatment market by End-user

11.6.5 Brazil

11.6.5.1 Brazil America Wheelchair by Product

11.6.5.2 Brazil America Wheelchair by Type

11.6.5.3 Brazil America Wheelchair by End-user

11.6.6 Argentina

11.6.6.1 Argentina America Wheelchair by Product

11.6.6.2 Argentina America Wheelchair by Type

11.6.6.3 Argentina America Wheelchair by End-user

11.6.7 Colombia

11.6.7.1 Colombia America Wheelchair by Product

11.6.7.2 Colombia America Wheelchair by Type

11.6.7.3 Colombia America Wheelchair by End-user

11.6.8 Rest of Latin America

11.6.8.1 Rest of Latin America Wheelchair by Product

11.6.8.2 Rest of Latin America Wheelchair by Type

11.6.8.3 Rest of Latin America Wheelchair by End-user

12. Company profile

12.1 Smith & Nephew plc.

12.1.1 Company Overview

12.1.2 Financials

12.1.3 Product/Services/Offerings

12.1.4 SWOT Analysis

12.1.5 The SNS View

12.2 Integra LifeSciences.

12.2.1 Company Overview

12.2.2 Financials

12.2.3 Product/Services/Offerings

12.2.4 SWOT Analysis

12.2.5 The SNS View

12.3 Hill-Rom Holdings, Inc.

12.3.1 Company Overview

12.3.2 Financials

12.3.3 Product/Services/Offerings

12.3.4 SWOT Analysis

12.3.5 The SNS View

12.4 Mélnlycke Health Care AB,

12.4.1 Company Overview

12.4.2 Financials

12.4.3 Product/Services/Offerings

12.4.4 SWOT Analysis

12.4.5 The SNS View

12.5 Essity Aktiebolag.

12.5.1 Company Overview

12.5.2 Financials

12.5.3 Product/Services/Offerings

12.5.4 SWOT Analysis

12.5.5 The SNS View

12.6 Cardinal Health.

12.6.1 Company Overview

12.6.2 Financials

12.6.3 Product/Services/Offerings

12.6.4 SWOT Analysis

12.6.5 The SNS View

12.7 3M.

12.7.1 Company Overview

12.7.2 Financials

12.7.3 Product/Services/Offerings

12.7.4 SWOT Analysis

12.7.5 The SNS View

12.8 B. Braun Melsungen AG.

12.8.2 Financials

12.8.3 Product/Services/Offerings

12.8.4 SWOT Analysis

12.8.5 The SNS View

12.9 Acelity LP,Inc.

12.9.1 Company Overview

12.9.2 Financials

12.9.3 Product/Services/Offerings

12.9.4 SWOT Analysis

12.9.5 The SNS View

12.10 Coloplast Group.

12.10.1 Company Overview

12.10.2 Financials

12.10.3 Product/Services/Offerings

12.10.4 SWOT Analysis

12.10.5 The SNS View

13. Competitive Landscape

13.1 Competitive Benchmarking

13.2 Market Share Analysis

13.3 Recent Developments

13.3.1 Industry News

13.3.2 Company News

13.3.3 Mergers & Acquisitions

14. Use Case and Best Practices

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Urinary Tract Infection Testing Market was valued at USD 625.23 million in 2023 and is expected to reach USD 1004.64 million by 2032, growing at a CAGR of 5.45% from 2024-2032.

The Surgical Retractors Market Size was valued at USD 2.12 billion in 2023 and is expected to reach USD 3.81 billion by 2032 and grow at a CAGR of 6.74% by 2024-2032.

Digital X-Ray Systems Market was valued at $ 7.9 billion in 2023 and is expected to reach $ 15.4 billion by 2032 and grow at a CAGR of 7.8% from 2024 to 2032.

The Soft Tissue Allograft Market size was valued at USD 5.11 billion in 2023 and is expected to reach USD 8.46 billion by 2032, with a growing at CAGR of 5.77% over the forecast period of 2024-2032.

The Bilirubin Blood Test Market Size was valued at USD 1.18 billion in 2023, and is expected to reach USD 2.11 billion by 2032, and grow at a CAGR of 6.7% over the forecast period 2024-2032.

The Home Infusion Therapy Market Size was valued at USD 35.98 Billion in 2023 and is expected to reach USD 71.82 Billion by 2032 and grow at a CAGR of 8.36% over the forecast period 2024-2032

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd